Dutch Pension Shift Obsessing Bond Traders Is About to Get Real

TL;DR

The €1.6 trillion Dutch pension system is shifting from bonds to riskier assets starting Jan. 1, potentially causing volatility in European bond markets. This could lead to higher long-term yields and a steeper yield curve, with market participants bracing for impact during low-liquidity holiday periods.

Key Takeaways

- •The Dutch pension system (€1.6 trillion) begins transitioning from bonds to riskier assets on Jan. 1, 2025, with €550 billion moving initially.

- •This shift could increase long-term bond yields, steepen the euro yield curve, and create market volatility, especially during holiday periods.

- •Market participants have been positioning for this change, with many reducing exposure to long-dated bonds and betting on yield curve steepening.

- •The transition creates uncertainty about timing and magnitude of bond sales, with Dutch funds having one year to adjust portfolios.

- •European governments face challenges as a major bond buyer becomes a seller, with some adjusting borrowing strategies in response.

Tags

One of the biggest owners of European government bonds could trigger a bout of volatility — just as many market participants are away from their desks.

In the European market for long-term bonds, a once-loyal and deep pocketed customer is about to start shopping elsewhere.

The €1.6 trillion ($1.9 trillion) Dutch pension system — the largest in the region — is undergoing a major transformation aimed at making it more sustainable for an aging population. Funds will invest more in riskier assets and less in bonds, with a big drop in demand expected for long-term interest-rate hedges.

The big start of the shift, years in the planning, is now just weeks away, with the first major tranche transitioning on Jan. 1. Around €550 billion in assets will move then, according to ING Bank NV, and outsized moves are more of a risk at a time of the year when many market participants tend not to be at their desks.

The sheer scale means central bankers and regulators have been fretting about how it will all play out. It’s also a huge issue for governments as stretched finances and increased public spending means they desperately need big buyers to soak up their debt.

Meanwhile, hedge funds and asset managers have been game-planning how to profit for much of this year. Many have dumped exposure to long-dated bonds and have piled into strategies that will pay out if they continue to underperform shorter-dated peers.

“Nothing has been talked about in European rates apart from Dutch pensions,” said Rohan Khanna, head of euro rates strategy at Barclays Plc. “It’s one of the most significant changes for European fixed income and most importantly, it’s a black box.”

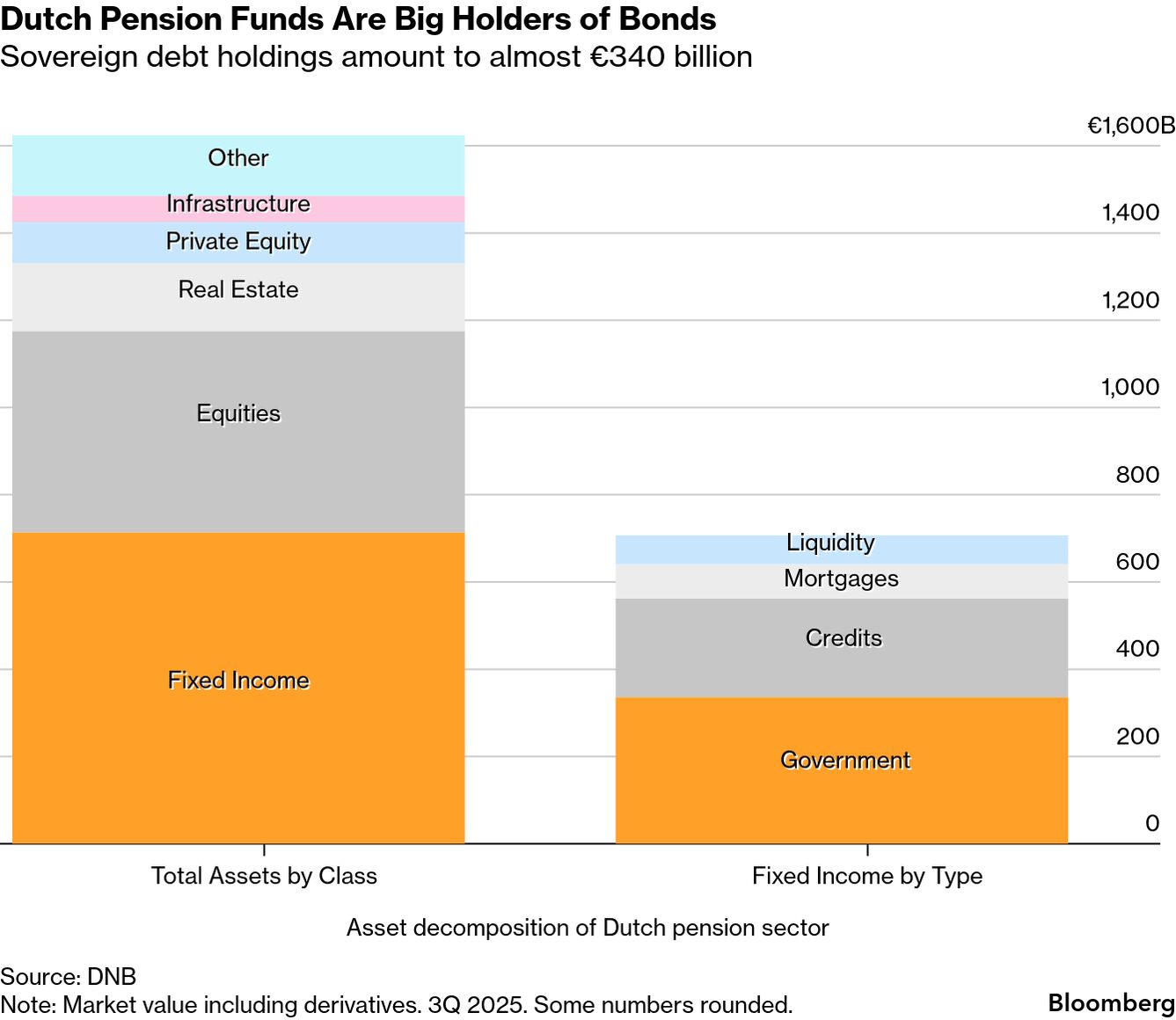

Sovereign debt holdings amount to almost €340 billion

Note: Market value including derivatives. 3Q 2025. Some numbers rounded.

The Dutch system is a whale in fixed income, holding about 65% of euro-area pension funds’ sovereign bonds, according to the European Central Bank. The size is related to the fact that occupational pension plans are mandatory for most workers.

Because these funds were so-called defined benefit schemes, they relied heavily on long-dated assets to ensure enough cash to pay retirees down the line.

But aging populations and declining birth rates means it’s getting harder to cover such costs, and the funds — in line with a long-term global trend — are changing to a system where payouts will depend on contributions and investment returns.

Funds will skew more toward risky assets and reduce exposure to bonds for people whose retirement is a long way off, and the balance will shift as clients age. They’ll need fewer interest-rate hedges, and the hedges they do implement will be shorter in duration.

Bond Sale

With such a big buyer turning into a seller, the end result is likely to be higher yields on longer-dated bonds and a steeper euro interest-rate swap curve — the products used for hedging. But the journey to get there could be jumpy.

Once the Dutch funds switch to new contracts, they’ll have a year to adjust their portfolios, in an attempt to lessen the risk of bottlenecks. That’s created a lot of uncertainty about exactly how much flow the market will see and when.

Some pensions have acknowledged there’ll be something of a learning-by-doing approach. PMT, the fund for the metal and engineering sector, estimates a six-month timeframe. It intends to move as quickly as possible, but a spokesperson said “market conditions in the first half year after this transition will be decisive for the pace.”

Read More:

- Dutch Pension Revamp Risks Turning Into a €2 Trillion Headache

- Dutch Pension Overhaul to Fuel Pivot From Long Bonds in EU

- Dutch Pension Changes Will Ripple Through Swap Market

- What Higher-for-Longer Bond Yields Mean for the World

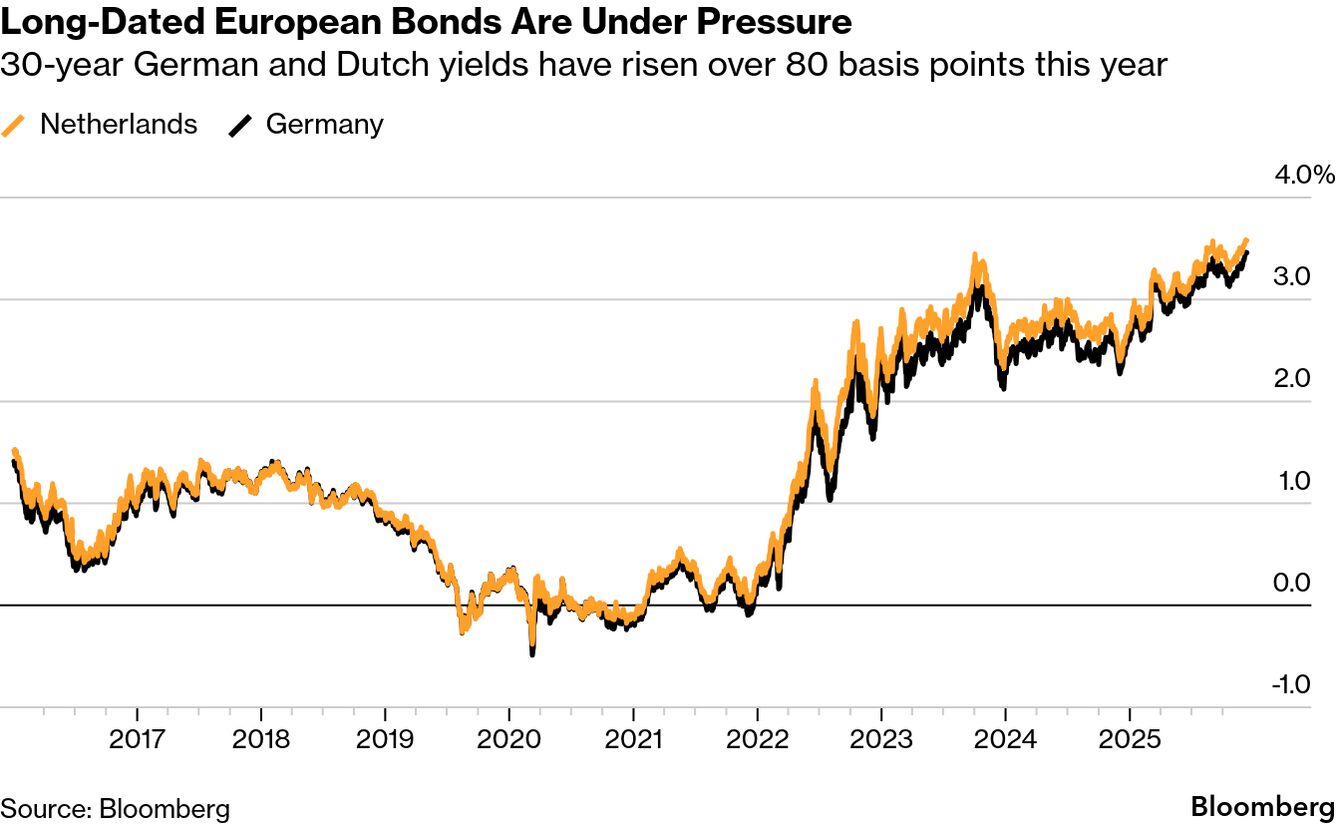

Anticipation of the Dutch transition, as well as ballooning government deficits, has made betting on a steeper yield curve one of the market’s favorite trades this year. Yields on Dutch and German 30-year bonds rose to the highest levels since 2011 late last week.

Given how much money is positioned, there’s even a risk of a sharp move in the opposite direction. If activity from Dutch pensions is underwhelming, or if other macro factors like the prospect of a euro-area interest-rate hike come back to the fore, that would hurt big bets on steepeners — which pay out if yields on long-term rates rise faster than those on shorter tenors — and prompt investors to swiftly bail out of the trade.

“The bulk of that move is now priced,” said Steve Ryder, senior portfolio manager at Aviva Investors. “We’re looking at heading into year-end still maintaining a steepening bias, but with a much reduced position.”

Many expect the biggest move to happen in the euro interest-rate swap curve. Insight Investment is positioned for it to steepen more than the German yield curve. Others including JPMorgan Asset Management continue to avoid exposure to long-dated European bonds.

The Dutch central bank and others have cautioned that low liquidity over the holiday period could lead to temporary market movements. Some trading desks plan to have higher than usual staffing to be ready for any volatility.

“I don’t know how many people are going to be working, but liquidity in the markets will be terrible,” said Ales Koutny, head of international rates at Vanguard, who is positioned for the yield curve to steepen.

30-year German and Dutch yields have risen over 80 basis points this year

Some see a selloff in European government bonds as a buying opportunity. UBS Asset Management contends long-dated German debt already looks good value on a long-term horizon and that yields may peak in January, given the significant supply coming from across Europe.

“If the Dutch pension funds push long-end yields higher, this would be an opportunity to get in,” said Kevin Zhao, head of global sovereign and currency at UBS Asset Management. “Treasury yields peaked around the second week of January last year, we think that this could play out in European rates next year.”

Euro-area countries are expected to issue a net total of €687 billion euros in government debt in 2026, according to rates strategists at Citigroup Inc. Almost €120 billion is coming in January alone.

As Dutch funds rebalance investment portfolios, government debt offices across Europe are acutely aware of — and adapting to — the looming supply and demand imbalance for long-dated bonds. The Netherlands is tilting its borrowing program toward shorter maturities, while Austria said it’s also prepared to modify its strategy.

“People are waiting with bated breath to see how it all plays out,” said Kal El-Wahab, head of EMEA linear rates trading at Bank of America. “There’s a lot of eyes and a lot of risk in this theme, it’s going to be an important next few weeks.”